What is E-invoicing

E-invoicing FAQs

1. What is e-invoicing?

E-Invoicing means issuing invoices electronically in a standard digital format that’s sent automatically between the seller, buyer, and the Tax Authority for validation, replacing paper or PDF invoices.

Is this information helpful?

2. What is the difference between paper invoices and e-invoices?

Paper invoices are issued manually and require signatures and stamps. E-invoices are issued digitally, are electronically certified, and carry a unique verification code.

Also, the e-invoices are issued and sent to the buyer and the Tax Authority instantly. They are stored electronically with instant verification and reporting, which is ensuring speed, accuracy, and security.

Is this information helpful?

3. What is the main objective of e-invoicing?

The main objective of e-invoicing is to improve business transaction efficiency, ensure transparency and tax compliance, as well as prevent fraudulent invoices.

Is this information helpful?

4. What are the direct benefits for companies?

Direct benefits for companies include reduced operating costs, simplified auditing, improved data accuracy and inventory management, reduced errors, integration with company systems, secure archiving, and real-time reporting for better decision-making.

Is this information helpful?

5.What are the implementation phases and who are the target groups?

The system will be implemented in 4 phases, each targeting a specific group as follows:

Phase 1: One hundred large VAT-registered companies, implementation begins in August 2026.

Phase 2: All large VAT-registered companies, implementation begins in February 2027.

Phase 3: All remaining VAT-registered taxpayers, implementation begins in August 2027.

Phase 4: Government institutions and entities, implementation begins in February (year to be announced)

Is this information helpful?

6. How were these Taxpayers selected?

Based on criteria such as revenue size, annual invoice volume, and technical readiness.

Is this information helpful?

7. Will SMEs be included?

Yes, within the third phase of the project. Can a company not targeted in the first phase applies the system voluntarily? Yes, optional early adoption is allowed with necessary support provided.

Is this information helpful?

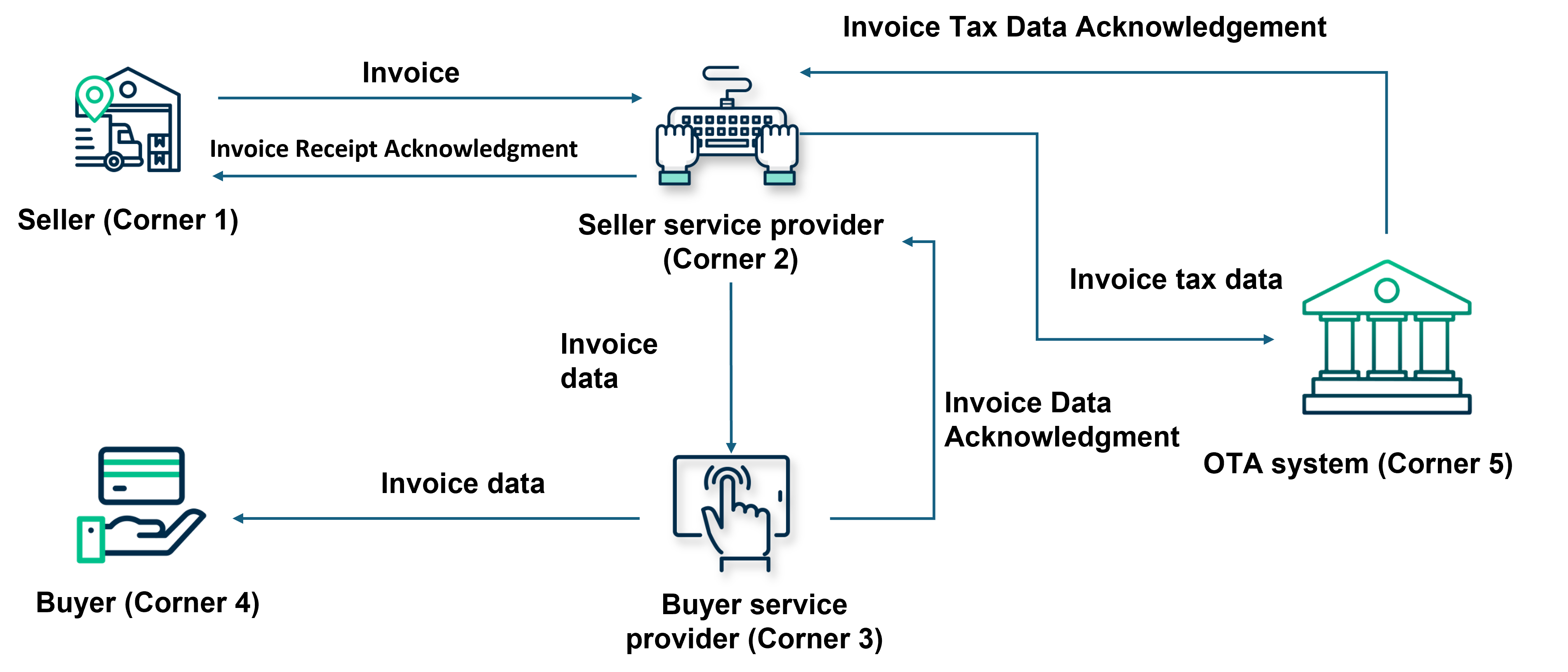

8. How is an e-invoice issued?

Invoices are issued through an electronic operating model linking taxpayers, service providers, tax system, and recipients to ensure secure and standardized issuance.

1. (Supplier)

2. (Supplier’s Service Provider)

3. (Buyer’s Service Provider)

4. (Buyer)

5. (Oman Tax Authority – OTA)

Is this information helpful?

Fawtara FAQ

PDF file